What I Learned Picking Inheritance Assets the Smart Way

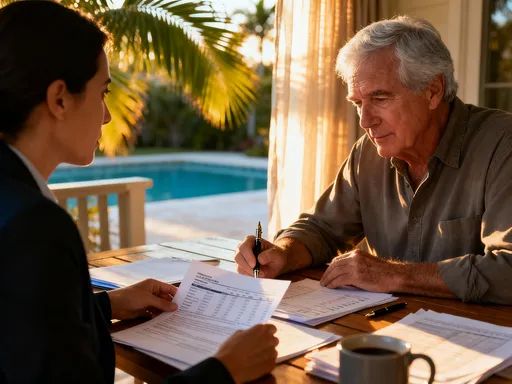

Planning for asset inheritance isn’t just about what you leave behind—it’s about how wisely you structure it. I’ve seen families struggle because of poor product choices, and I made mistakes too. After navigating tax traps and liquidity issues, I discovered strategies that balance growth, access, and protection. This is a real talk on selecting financial products not for short-term gains, but for lasting legacy—without overcomplicating it or falling for flashy promises. It’s not about leaving more; it’s about ensuring what you leave actually helps, lasts, and doesn’t become a burden. The difference between a meaningful inheritance and a complicated mess often comes down to one thing: choosing the right financial products with clarity and purpose.

The Hidden Challenge of Passing Down Wealth

Inheritance is often viewed as a straightforward transfer of money, property, or investments from one generation to the next. Yet, the reality is far more complex. Many people assume that building a large estate automatically ensures their family’s future security. However, without careful planning, even substantial wealth can diminish rapidly after death due to avoidable structural flaws. The true challenge lies not in accumulating assets, but in preserving their value so they serve the next generation as intended. This requires understanding the systems, timelines, and hidden costs that come into play when wealth changes hands.

One of the most common oversights is the role of probate—the legal process through which a will is validated and assets are distributed. While necessary in many cases, probate can be time-consuming and expensive. Estates that rely solely on wills often face delays of months or even years before beneficiaries receive anything. During this period, assets may lose value, especially if markets decline or properties require maintenance. Legal fees, court costs, and executor charges further erode the estate’s worth. For families already dealing with emotional loss, these financial complications add unnecessary stress and uncertainty. What was meant to provide stability instead becomes a source of strain.

Tax inefficiencies present another silent threat. Depending on jurisdiction, inherited assets may trigger estate taxes, inheritance taxes, or capital gains taxes. These levies can consume a significant portion of the estate, particularly if assets are held in taxable accounts or if no tax-minimization strategy was implemented during the owner’s lifetime. For example, appreciated stocks passed through a standard brokerage account might be subject to capital gains tax when sold by the heir, even if no tax was paid when originally acquired. Without planning, heirs inherit not just wealth—but tax liabilities.

Equally important is the mismatch between asset types and family needs. A family home may hold deep sentimental value, but if it’s the largest asset in the estate and the heirs cannot afford ongoing taxes or maintenance, it may have to be sold anyway. Similarly, a business interest may represent years of hard work, but transferring ownership without a succession plan can lead to operational collapse. Emotional attachments often lead people to preserve certain assets at the expense of practicality, resulting in decisions that feel right in the moment but create long-term hardship. The key is to move beyond sentiment and evaluate each asset based on its functionality within the broader inheritance strategy.

Why Product Choice Matters More Than You Think

When it comes to inheritance planning, the specific financial products used can have a greater impact than the total amount of wealth accumulated. A high-return investment may look impressive on paper, but if it lacks liquidity or clear transfer mechanisms, it can become more of a liability than a gift. The right product is not necessarily the one with the highest historical performance, but the one that aligns with the family’s long-term needs for access, control, and tax efficiency. This shift in perspective—from return-focused to purpose-driven selection—is essential for building a durable legacy.

Take life insurance, for example. While it doesn’t generate investment returns in the traditional sense, certain permanent life insurance policies offer tax-free death benefits and can serve as a reliable source of immediate liquidity. This means heirs can cover estate taxes, funeral costs, or other expenses without having to liquidate other assets at an inopportune time. Additionally, life insurance proceeds bypass probate when properly structured, allowing for faster distribution. In contrast, a large stock portfolio, while potentially valuable, may require time to sell and settle, delaying access when funds are most needed.

Trusts represent another powerful tool, offering greater control over how and when assets are distributed. Unlike a will, which typically transfers assets outright upon death, a trust can specify conditions—such as age milestones or educational achievements—before distributions occur. This helps protect inheritances from being misused, especially if beneficiaries are young or lack financial experience. Revocable living trusts also avoid probate, reducing both time and legal costs. However, setting up a trust involves upfront effort and legal fees, making it more suitable for estates with complexity or specific goals.

Mutual funds and exchange-traded funds (ETFs) offer a different kind of advantage: simplicity and diversification. These investment vehicles allow heirs to inherit a balanced portfolio without the burden of managing individual stocks or bonds. Low-cost index funds, in particular, have proven to deliver strong long-term returns with minimal management, making them ideal for passive investors who may not have the time or expertise to actively manage inherited assets. In contrast, actively managed funds often come with higher fees and inconsistent performance, which can drag down returns over time.

Real estate, while often seen as a cornerstone of wealth, presents unique challenges. Properties may appreciate in value, but they also require ongoing maintenance, property taxes, and potential management. If multiple heirs inherit a property, disagreements over usage or sale can lead to conflict. Holding real estate within a limited liability company (LLC) or transferring it through a trust can help mitigate these risks, but such strategies require advance planning. The lesson is clear: the best financial products for inheritance are those that combine growth potential with ease of transfer, cost efficiency, and alignment with the family’s practical and emotional needs.

Balancing Growth and Liquidity for Future Generations

One of the most overlooked aspects of inheritance planning is the balance between growth and liquidity. It’s natural to focus on maximizing investment returns, but without sufficient liquid assets, heirs may face serious financial pressure immediately after a loved one’s passing. Estate taxes, legal fees, outstanding debts, and ongoing household expenses do not wait for markets to recover or properties to sell. If the estate lacks accessible cash, heirs may be forced to liquidate long-term investments at a loss, undermining years of careful wealth building.

Consider a scenario where a family inherits a portfolio heavily concentrated in real estate and private business interests. On paper, the estate appears valuable, but none of the assets can be quickly converted to cash. Meanwhile, the government demands payment of estate taxes within nine months. With no ready funds, the heirs must sell property or business shares—possibly during a market downturn—just to meet obligations. The result is a significant reduction in overall wealth, not because the assets were poorly chosen, but because the structure failed to account for short-term liquidity needs.

To prevent this, it’s essential to incorporate liquid instruments into the inheritance plan. These include cash accounts, money market funds, short-term bonds, and certain insurance products that provide immediate access to funds. One effective strategy is to maintain a dedicated “bridge account” funded with low-risk, highly liquid assets. This account can cover immediate expenses for six to twelve months, giving heirs time to assess their options without making rushed financial decisions. Another approach is to use staggered maturity bonds or certificates of deposit (CDs), which provide predictable cash flow at regular intervals.

Life insurance also plays a critical role in liquidity planning. A permanent policy with a death benefit can deliver a tax-free lump sum precisely when it’s needed most. This money can be used to pay taxes, settle debts, or support dependents without disrupting the long-term investment portfolio. For business owners, life insurance can fund a buy-sell agreement, ensuring a smooth transition of ownership without forcing the sale of the company. The key is to view insurance not as an investment vehicle, but as a financial safety net that preserves the integrity of other assets.

Another often-underutilized tool is the use of payable-on-death (POD) accounts or transfer-on-death (TOD) registrations for brokerage accounts. These designations allow assets to pass directly to named beneficiaries without going through probate, enabling faster access to funds. While simple to set up, they provide a level of control and speed that traditional estate planning methods cannot match. By combining these liquid solutions with long-term growth investments, families can create a balanced inheritance structure that supports both immediate needs and future prosperity.

Tax Efficiency: Protecting Value Before It’s Passed On

Taxes are one of the largest expenses an estate will ever face, yet many people fail to plan for them until it’s too late. Depending on the size of the estate and the jurisdiction, tax rates can reach 40% or more, significantly reducing what heirs ultimately receive. The good news is that with thoughtful product selection and account structuring, much of this tax burden can be minimized. The goal is not to avoid taxes illegally, but to use legitimate financial tools that align with tax laws to preserve more of the wealth for the next generation.

One of the most important concepts in tax-efficient inheritance is the stepped-up basis. When certain assets, such as stocks or real estate, are inherited, their cost basis is adjusted to the market value at the time of death. This means that if the heir later sells the asset, they only pay capital gains tax on the appreciation that occurred after inheritance, not on the gains accumulated during the original owner’s lifetime. This can result in substantial tax savings, especially for long-held, highly appreciated assets. However, this benefit only applies to assets held in taxable accounts and transferred directly to heirs—not to those passed through retirement accounts like traditional IRAs or 401(k)s.

Retirement accounts present a different set of rules. Distributions from these accounts are generally taxed as ordinary income, and recent changes to the law require most non-spouse beneficiaries to withdraw all funds within ten years. This can push heirs into higher tax brackets, especially if large withdrawals are made in a single year. To mitigate this, some individuals choose to gradually convert traditional IRAs to Roth IRAs during their lifetime, paying taxes at their current rate in exchange for tax-free growth and withdrawals for heirs. While this strategy requires upfront tax payment, it can lead to significant long-term savings for the next generation.

Holding assets in the right type of account is equally important. Taxable brokerage accounts offer flexibility and access to the stepped-up basis, while tax-deferred accounts like traditional IRAs grow without annual taxation but create future tax liabilities. Tax-free accounts, such as Roth IRAs and certain life insurance policies, offer the greatest advantage for heirs because they allow tax-free growth and withdrawals. By strategically allocating assets across these account types—a practice known as asset location—individuals can optimize the tax efficiency of their estate.

Charitable giving can also play a role in tax planning. Donating appreciated stock directly to a qualified charity avoids capital gains taxes and provides a charitable deduction. For those with large IRAs, naming a charity as the beneficiary can eliminate income tax on the account while leaving other, more tax-efficient assets to heirs. These strategies demonstrate that tax efficiency is not about hiding money, but about using the tax code wisely to protect and direct wealth according to one’s intentions.

Avoiding the Trap of Overconcentration

Many individuals accumulate the majority of their wealth in a single asset—most commonly their home or a family business. While this can be a natural result of career focus and long-term investment, it creates significant risk for heirs. Overconcentration means that the financial well-being of the next generation depends on the performance and stability of just one asset. If that asset declines in value, faces regulatory challenges, or becomes difficult to manage, the entire inheritance is jeopardized.

Consider the case of a business owner who poured decades of effort into building a successful company. The business represents nearly all of the estate’s value. Upon retirement or passing, the children are expected to take over. But what if they lack interest, experience, or agreement on how to run it? Without a succession plan, the business may falter, lose key employees, or be sold at a fraction of its potential value. Similarly, a home that has appreciated significantly may seem like a valuable inheritance, but if property taxes, maintenance, and insurance consume a large portion of the heirs’ income, it can become a financial burden rather than a blessing.

The solution lies in diversification—spreading wealth across different asset classes to reduce risk. This doesn’t mean abandoning the family home or business, but gradually reallocating a portion of the wealth into other investments such as stocks, bonds, real estate investment trusts (REITs), or low-cost index funds. Diversification helps ensure that if one asset underperforms, others can help maintain overall financial stability. It also provides heirs with more options—whether that’s pursuing education, starting a business, or buying a home of their own.

For business owners, tools like partial sales, employee stock ownership plans (ESOPs), or exchange funds can help reduce concentration without losing control. An exchange fund, for example, allows owners of concentrated stock positions to pool their shares with others and receive diversified ownership in return. This provides exposure to a broader market while deferring capital gains taxes. Similarly, gradually gifting portions of the business or real estate to heirs over time can reduce estate size and transfer wealth in a tax-efficient manner.

The goal is not to eliminate meaningful assets, but to ensure they are part of a balanced portfolio. By addressing overconcentration early, individuals can protect their legacy from being wiped out by a single adverse event. It’s a proactive step that reflects both financial wisdom and care for the next generation’s long-term security.

Tools That Work: Real Uses of Trusts, Insurance, and Funds

Theoretical knowledge is valuable, but real-world application is what makes a difference. When it comes to inheritance planning, certain financial tools have consistently proven their worth through practical use. Trusts, insurance, and investment funds are not just abstract concepts—they are functional instruments that, when used correctly, can simplify transfer, reduce costs, and protect wealth. Understanding how each works in real scenarios helps families make informed choices that align with their unique circumstances.

Revocable living trusts are among the most effective tools for avoiding probate and maintaining privacy. Unlike a will, which becomes public record after death, a trust remains private and allows for immediate transfer of assets to beneficiaries. This is particularly useful for families who value discretion or have complex asset structures. A trust also enables the grantor to retain control during life, with the ability to amend or revoke it at any time. Upon death, a successor trustee takes over, distributing assets according to the trust’s terms without court involvement. This can save months of waiting and thousands in legal fees.

Life insurance, particularly permanent policies such as whole life or universal life, serves multiple purposes beyond death benefits. In addition to providing tax-free liquidity, some policies accumulate cash value that can be borrowed against during life. This feature can be useful for covering unexpected expenses or supplementing retirement income. For estate planning, the death benefit can be structured to pay estate taxes, preventing heirs from having to liquidate other assets. When held in an irrevocable life insurance trust (ILIT), the proceeds are excluded from the taxable estate, enhancing tax efficiency.

Investment funds, especially low-cost index funds, offer a practical solution for heirs who may not have the time or expertise to manage individual securities. Actively managed funds often come with high expense ratios and inconsistent performance, which can erode returns over time. In contrast, index funds track broad market benchmarks with minimal fees, delivering reliable long-term growth. For heirs who prefer a hands-off approach, these funds provide a stable foundation for inherited wealth. Additionally, holding funds in tax-efficient accounts like Roth IRAs or taxable brokerage accounts enhances their long-term value.

The effectiveness of these tools depends on proper setup and ongoing review. A trust must be properly funded—meaning assets are legally transferred into it—to be effective. Life insurance policies should be reviewed periodically to ensure coverage remains adequate and premiums are affordable. Investment accounts should be rebalanced as needed to maintain alignment with goals. By treating these tools as living components of a financial plan, rather than one-time decisions, families can ensure they continue to serve their purpose across generations.

Building a Legacy, Not Just Leaving Assets

True wealth transfer is about more than numbers on a balance sheet. It’s about values, preparation, and the ability of the next generation to use what they inherit wisely. A well-structured estate plan ensures that assets are preserved and transferred efficiently, but it’s equally important to prepare heirs for their new responsibilities. Without financial literacy or clear expectations, even the most carefully planned inheritance can be squandered.

One of the most effective ways to build a lasting legacy is to involve heirs in the planning process early. This doesn’t mean sharing every detail, but providing education about the family’s financial values, goals, and the purpose behind certain decisions. Open conversations about money reduce surprises and help heirs understand that wealth is a tool, not a guarantee of comfort. Some families hold regular meetings to discuss financial matters, creating a culture of transparency and responsibility.

Setting clear expectations is equally important. If certain assets are intended to remain in the family for generations, such as a vacation home or business, those intentions should be communicated clearly. Trusts can be used to formalize these wishes, but without dialogue, even the best legal structure may be ignored or contested. The goal is to align legal tools with family values, ensuring that the plan reflects not just financial logic, but emotional and ethical considerations as well.

Ultimately, smart inheritance planning is not about complexity, but intentionality. It’s about choosing the right products—not for their returns alone, but for how they support access, control, tax efficiency, and long-term stability. It’s about preparing heirs not just to receive wealth, but to steward it wisely. By focusing on purpose over profit and clarity over convenience, families can create a legacy that endures not just in value, but in meaning.